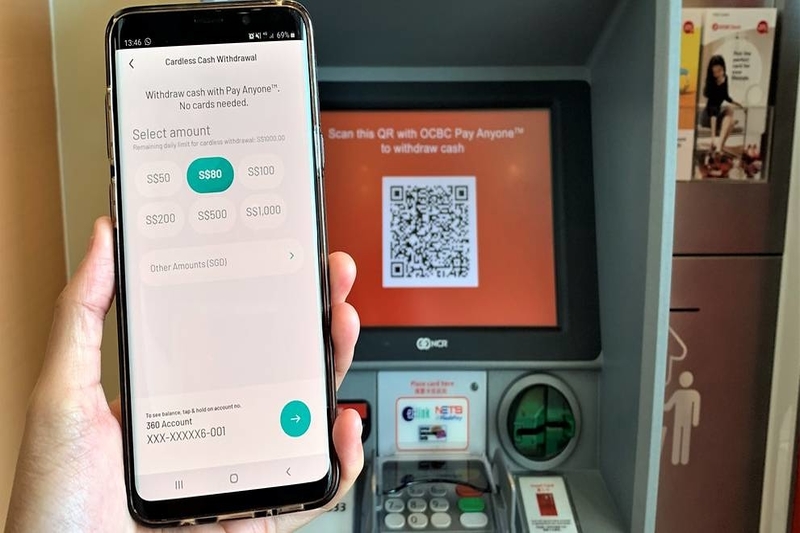

OCBC Bank is offering an alternative process for the withdrawal of money for their customers. They have established a system of using QR codes.

Customers can download and use the OCBC Pay Anyone app to scan a QR code, which is followed by a fingerprint, faceprint or mobile banking login credentials for the authentication of the transaction.

OCBC has said that it is the first bank to implement such a procedure.

It has stated that using a QR code is “more secure” than a PIN number.

“Using a QR code instead of keying in a PIN is more secure because biometric authentication can be chosen – which is a more robust security feature than a PIN number that can be revealed or stolen,” said OCBC.

It added that while a physical ATM card can be stolen and used, stealing a mobile device would be much pointless as one will be barred from accessing the customer’s bank account due to the need for the fingerprint or faceprint authentication.

This new process will also shorten the average time spent at ATM stations from 80 to 45 seconds.

Aditya Gupta, head of OCBC’s digital business for Singapore and Malaysia said, “As we accelerate our drive to go cashless, we also recognise that ATMs are still an essential and frequently used touchpoint for our customers.”

He said that there is a growing number of customers who are used to or understand the process of QR code scans.

As of now, 655 OCBC ATMs have this QR-code scanning cash withdrawal service.

While this is a new development in the use of QR codes for cash withdrawal, payment using this technology has been in practice for a while.

OpenGov had earlier reported that the Payments Council has agreed to develop a common QR code for Singapore known as “SGQR”.

Council members for the new taskforce developing this code had advocated that the use of QR code-based payments as a practical and convenient way to introduce e-payments to cash-based merchants.

A common QR code will help facilitate Singapore’s move towards a cashless society. This is in line with one of the national strategic projects under Singapore’s Smart Nation plans.

While debit and credit card schemes worked well for large merchants and retailers, these solutions were often not feasible for smaller merchants who prefer an infrastructure-light and cheaper solution.

As the increase in usage of QR code payments posed a risk of fragmented payments for merchants and inefficient transactions between consumers and merchants, a common QR code will solve these issues. It can be used to facilitate payment among different payment schemes, e-wallets and banks.