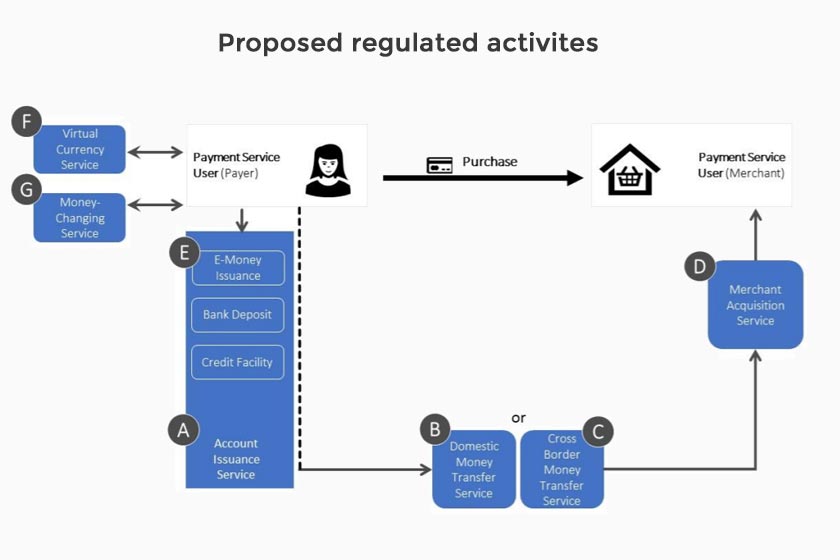

Image credit: MAS (From Consultation Paper on the Proposed Payment

Services Bill, page 12)

The Monetary Authority of Singapore (MAS) has launched

a second consultation on its proposed payments regulatory framework, known as the

Payment Services Bill (the

Bill). The public consultation will run from 21 November 2017 to 8 January

2018.

The Bill will streamline the regulation of payment services

under a single legislation, expand the scope of regulated payment activities to

include virtual currency services and other innovations, and calibrate

regulation according to the risks posed by these activities.

Last year, MAS had sought

public feedback on the scope of the proposed payments regulatory framework. MAS

has considered and responded

to the feedback received.

When the new Bill is enacted, payment firms will only need

to hold one licence under a single regulatory framework to conduct any or all

of the specified payment activities. There will be three classes of licences

that an entity can apply for under the Bill. A payment service provider may

apply to be a a) Money-Changing Licensee; b) Standard Payment Institution, or

c) Major Payment Institution.

The single licence will permit a licensee to undertake

specific activities as set out in its licence. Multiple licences will not be

required for different payment activities. If the licensee conducts more

payment activities than originally applied for, it must seek MAS’ approval to

conduct other payment activities.

Only payment activities that face customers or merchants,

process funds or acquire transactions, and pose relevant regulatory concerns

will need to be licensed.

The new framework will expand the scope of regulation to

include domestic money transfers (e.g. transferring money through payment

kiosks), merchant acquisition (e.g. acquiring transactions through a

point-of-sale terminal or online payment gateway), and the purchase and sale of

virtual currencies.

MAS wants to ensure that the expanded scope of regulation is

not onerous. To do so, the Bill will differentiate regulatory requirements

according to the risks that specific payment activities pose rather than apply

a uniform set of regulations on all payment service providers.

For instance, MAS proposes to exclude smaller entities from

requirements on technology risk, user protection, and interoperability

requirements, and only subject them to AML/CFT and general requirements.

The Bill will empower MAS to regulate payment services for

money-laundering and terrorism financing risks, strengthen safeguards for funds

belonging to consumers and merchants, set standards on technology risk

management and enhance interoperability of payment solutions across a wider

range of payment activities.

MAS is seeking comments on 23 questions in the consultation

document, on issues such as whether

the definitions of e-money and virtual currency accord with industry

understanding of these terms and whether the description of the activities

excluded from financial regulation is sufficiently clear and whether more

activities should be excluded.

Other matters being explored include the proposed single

licence structure and and whether this approach is beneficial for potential

licensees, the proposed capital and security deposit requirements, the AML/CFT (anti-money

laundering/ countering the financing of terrorism) requirements and the interoperability

powers (MAS is proposing to include in the Bill powers to mandate any Major

Payment Institution to adopt a common standard to make widely used payment

acceptance methods interoperable. One example of such a measure is to mandate

that payment account issuers and merchant acquirers adopt a standardised

QR code.)

MAS is also inviting payment users to give feedback on the

proposed payment user

protection measures.

MAS Managing Director, Mr. Ravi Menon said, “We want to put

in place a forward-looking regulatory regime to encourage wider adoption of

secure e-payment solutions. The novel, activity-based licensing framework aims

to right-size regulatory requirements to address the risks posed by specific

payment activities. This will help to protect consumers and merchants while

creating an environment conducive for innovation in payment services.”